Reminder for CPAs: Confirm the List of Audit Clients Signed Before 30 June 2026

The Federation of Accounting Professions reminds Certified Public Accountants who perform audit engagements to report and confirm the list of entities for which they have signed the auditor’s report through the TFAC system.

For 2026, CPAs who signed auditor’s reports during the period from 1 January to 30 June 2026 are required to confirm their signing information by 30 June 2026.

Before confirmation, key information such as the signing year, company registration number, accounting period-end date, and auditor’s report date should be carefully reviewed.This confirmation process is not merely an administrative step. It is part of audit quality control and professional transparency.

It also helps ensure that information in the DBD e-Filing system and TFAC’s auditor system is consistent, reducing the risk of signature forgery or misuse of a CPA’s name.Failure to report and confirm the entities for which the CPA has signed may be considered non-compliance with TFAC requirements and may lead to the ethics enforcement process for professional accountants.

For companies undergoing an annual audit, selecting an auditor who follows professional and compliance procedures properly is important. Proper post-signing compliance reflects the quality, transparency, and credibility of the audit work.

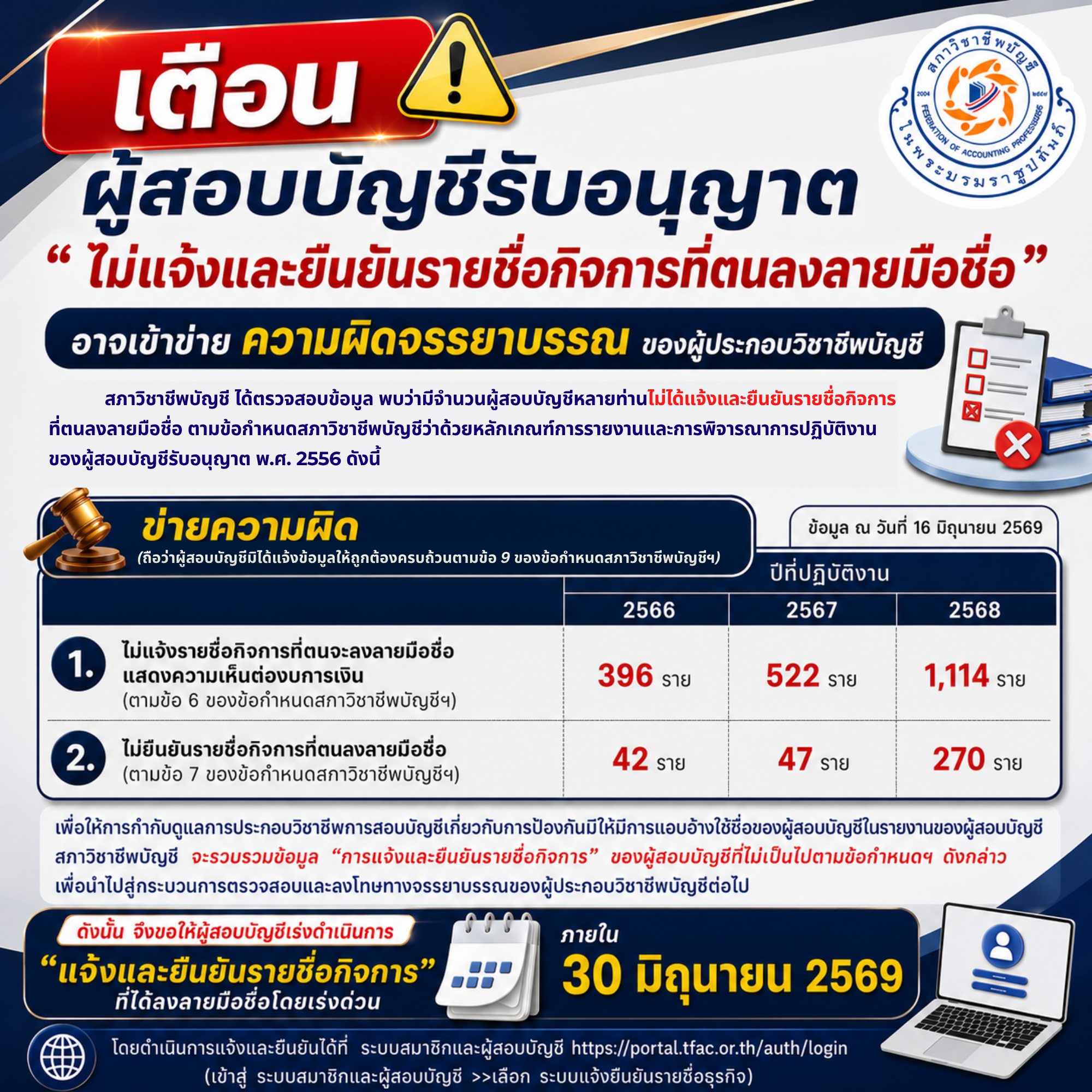

เตือนผู้สอบบัญชีรับอนุญาต: อย่าลืมแจ้งและยืนยันรายชื่อกิจการที่ลงลายมือชื่อ

สภาวิชาชีพบัญชีเตือนผู้สอบบัญชีรับอนุญาตที่ปฏิบัติงานสอบบัญชีว่า ต้องแจ้งและยืนยันรายชื่อกิจการที่ตนลงลายมือชื่อในรายงานของผู้สอบบัญชีรับอนุญาตให้ถูกต้องและครบถ้วนผ่านระบบของสภาวิชาชีพบัญชี

สำหรับปี 2569 ผู้สอบบัญชีรับอนุญาตที่ลงลายมือชื่อระหว่างวันที่ 1 มกราคม ถึง 30 มิถุนายน 2569 ต้องแจ้งยืนยันการลงลายมือชื่อภายในวันที่ 30 มิถุนายน 2569 โดยควรตรวจสอบข้อมูลสำคัญ เช่น ปีที่ลงลายมือชื่อ เลขทะเบียนนิติบุคคล วันสิ้นรอบบัญชี และวันที่ลงลายมือชื่อ ให้ถูกต้องก่อนยืนยัน

การแจ้งและยืนยันรายชื่อกิจการไม่ใช่เพียงขั้นตอนทางเอกสาร แต่เป็นส่วนหนึ่งของการควบคุมคุณภาพและความโปร่งใสของงานสอบบัญชี ช่วยให้ข้อมูลของผู้สอบบัญชีในระบบ DBD e-Filing และระบบของสภาวิชาชีพบัญชีสอดคล้องกัน และช่วยลดความเสี่ยงจากการถูกแอบอ้างหรือปลอมแปลงลายมือชื่อ

หากผู้สอบบัญชีรับอนุญาตไม่แจ้งและยืนยันรายชื่อกิจการที่ตนลงลายมือชื่อ อาจถือว่าไม่ปฏิบัติตามข้อกำหนดของสภาวิชาชีพบัญชี และอาจเข้าข่ายถูกดำเนินการตามกระบวนการบังคับใช้จรรยาบรรณของผู้ประกอบวิชาชีพบัญชี

สำหรับบริษัทที่ได้รับการตรวจสอบงบการเงิน ควรเลือกผู้สอบบัญชีที่ปฏิบัติงานอย่างถูกต้อง โปร่งใส และดูแลขั้นตอน compliance หลังการลงลายมือชื่อครบถ้วน เพราะสิ่งเหล่านี้สะท้อนถึงคุณภาพและความน่าเชื่อถือของงานสอบบัญชี

External References

- Federation of Accounting Professions — Reminder for CPAs to confirm audit signing for 2026https://www.tfac.or.th/en/Article/Detail/184283

- Federation of Accounting Professions — DBD e-Filing alert function for auditor signing informationhttps://www.tfac.or.th/Article/Detail/157118

- TFAC Online Servicehttps://www.tfac.or.th/